China’s trading partners are once again fretting about the country’s supposedly unfair economic practices. This time, the focus is on China’s alleged attempt to export its excess capacity, especially in emerging sectors such as electric vehicles (EVs), and to undermine domestic industries in the United States and Europe.

But before the world embarks on the next round of retaliatory action against China, it is critical to understand the stubborn, even mystifying, resilience of the Chinese export juggernaut. As my co-authors and I document in a recent paper, China’s share of global exports has continued to soar, despite other countries’ more restrictive trade responses and domestic actions that should have corrected the imbalance. This paradox has serious policy implications.

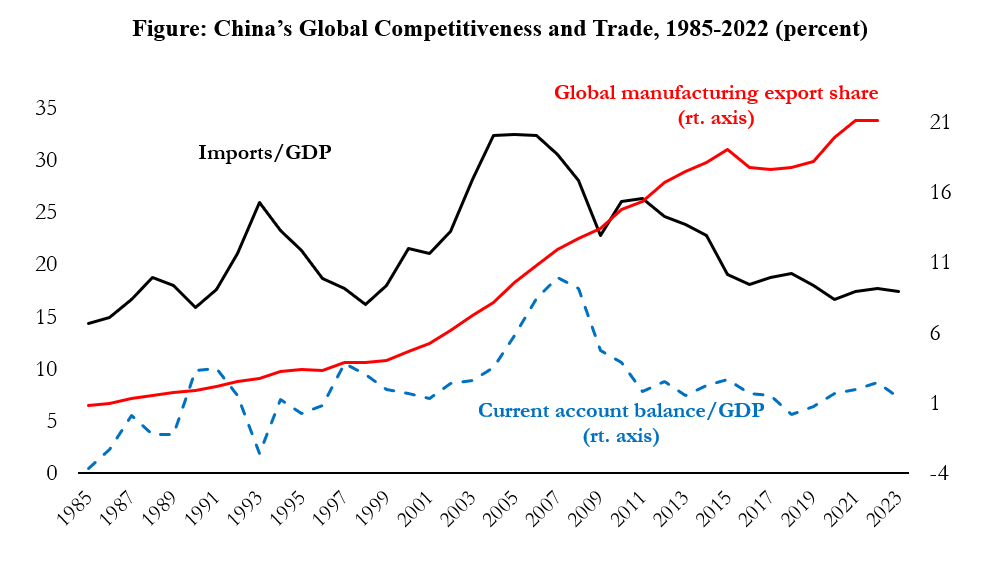

The figure below shows the role of trade in China’s exceptional economic performance over recent decades. From the mid-1980s until the global financial crisis (GFC) of 2008, the ratio of China’s imports to GDP more than doubled, from roughly 14% to around 33%. But China’s current-account balance (the excess of exports over imports) swung from a deficit of 4% of GDP to a surplus of nearly 10%.

These two outcomes reflected China’s opening to the outside world. A rising import-to-GDP ratio typically results from trade liberalization, including the reduction of tariff and non-tariff barriers. China famously shed its inward orientation after Deng Xiaoping’s reforms, culminating in the country’s accession to the World Trade Organization in 2001.

At the same time, rising current-account surpluses can be traced to China’s aggressive export-promotion strategy, which entailed the government keeping the economy closed to foreign capital inflows and the central bank buying surplus foreign currency to maintain a competitive exchange rate. As a result, foreign-exchange reserves ballooned, peaking at $4 trillion.

Trade openness and aggressive mercantilism then contributed to a third outcome: China’s steadily increasing share of global exports. In particular, its share of global manufacturing exports rose from less than 1% in 1985 to 12% by 2007, reaching astronomical levels of up to 50% in sectors such as apparel and footwear. In other words, trade and other policies produced faster manufacturing-sector productivity growth in China compared to the rest of the world.

China’s rising exports and current-account surpluses provoked anxiety in America and elsewhere, triggering a series of policy responses. First, facing pressure from the US, China began allowing the renminbi to appreciate against the dollar right before the GFC. The currency strengthened by around 50% over a decade, and the country’s current-account surplus fell from a peak of 10% of GDP in 2006 to virtually zero in 2018.

Second, China embarked on a massive stimulus in the years after the GFC, financing a real estate and infrastructure boom. This shift in public spending tilted the composition of output toward non-tradables. Third, under President Xi Jinping, China started turning inward, emphasizing “localization” and “internal circulation” which aimed to restrict foreign competition in the Chinese economy. Lastly, the US under former President Donald Trump hiked tariffs against China, a strategy that President Joe Biden has pursued even more aggressively.

These measures – a large and sustained currency appreciation, ambitious government spending, and aggressive protectionist measures – should have undermined China’s competitiveness. It makes intuitive sense that a stronger renminbi and America’s protectionist turn should have reduced China’s exports. And in more subtle, but no less important, ways, Chinese protectionism and stimulus should have had the same effect.

The collapse of imports after the GFC should have impeded export competitiveness, according to the economist Abba Lerner’s view that “an import tax is an export tax.” And the relative boom in non-tradables caused by the stimulus should have undermined the competitiveness of the tradable sector because of rising wages and price inflation domestically (also known as the Balassa-Samuelson effect). But none of this happened. The march of the Chinese export juggernaut has been relentless, with China’s share of global manufacturing exports jumping from 12% around the GFC to 22% by 2022.

Now, China’s current-account surplus is soaring again (despite being obscured by flawed data, as Brad Setser of the Council on Foreign Relations has shown), and its currency is weakening. Pressure is mounting on the US and Europe to take retaliatory action.

But the first step should be understanding this paradox of China’s globalization, namely, why exports have defied the corrective effects of conventional policy levers. For example, China may be massively subsidizing its exports, but in an unconventional or concealed manner. Or it could be that Chinese firms have been very efficient, especially in mastering new technologies in sectors such as EVs. The US and Europe should be discussing these issues with China, tailoring responses to the underlying diagnosis, rather than taking knee-jerk protectionist measures that serve only to stoke tensions.

Copyright: Project Syndicate, 2024.

www.project-syndicate.org