Despite ongoing predictions of its decline, the U.S. dollar remains dominant—but rising debt, political instability, and market volatility are shaking investor confidence. If these trends persist, the world could shift toward a more fragmented and unstable multipolar monetary system.

Over past decades, many economists, pundits, and analysts predicted the end of King Dollar, the dominance of the American currency in global payments and reserves. But thus far, not one prediction has come true. The U.S. dollar never faced challenges to its decades-long position as the main global reserve currency, remaining the best alternative among possible currency contenders.

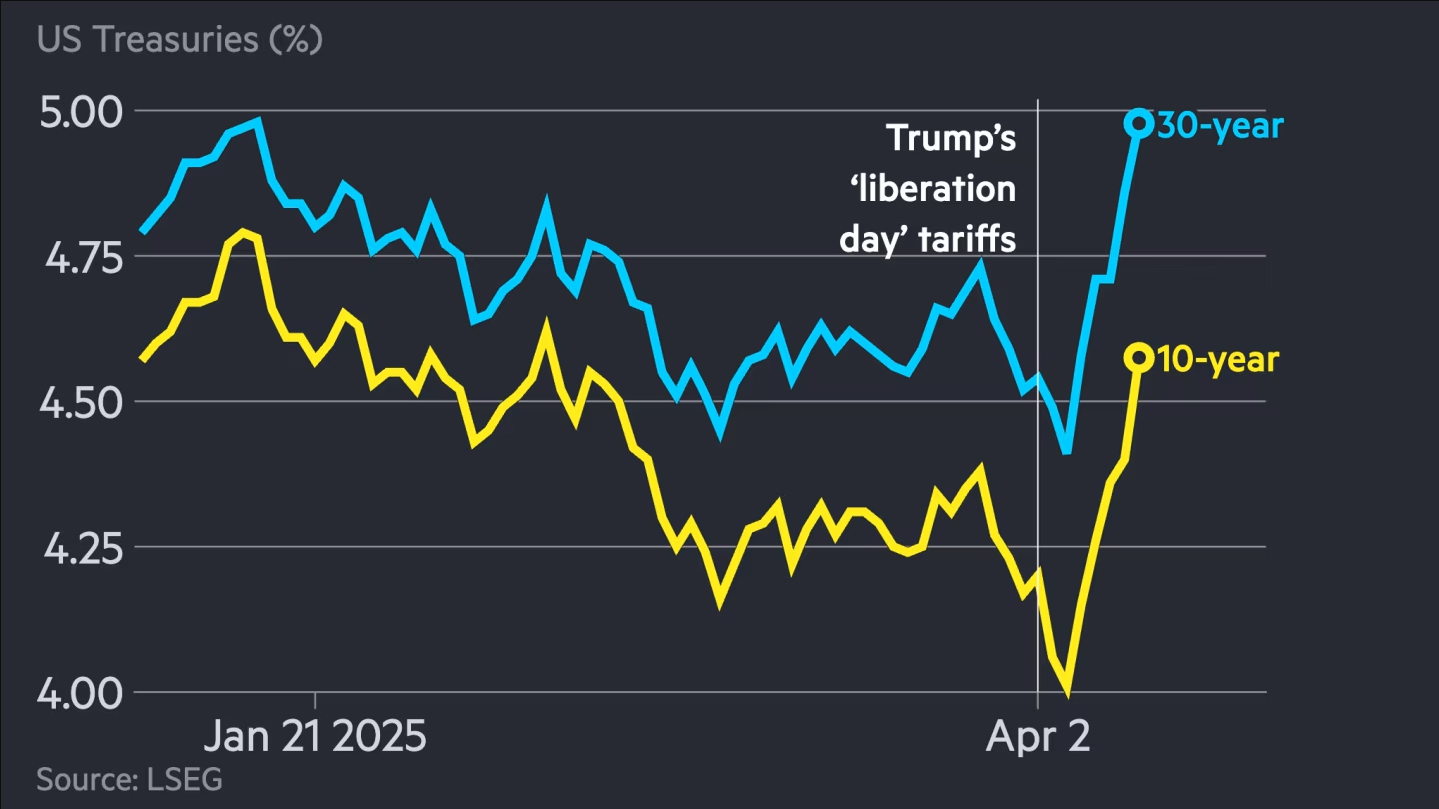

Is this time different? What has been termed a “freak sell-off” in the U.S. Treasuries market is raising doubts as to how secure America’s IOUs truly are. While the stock market has been making the headlines, Trump acknowledged that the bond market played a role in his massive U-turn on global tariffs ex-China on April 9, saying investors “were getting a little queasy.” Continued selling of U.S. government bonds raised the risk of freezing or dislocating the market.

This situation is not normal. Over the past fifty plus years of freely floating currencies, the U.S. dollar has acted as a “safe haven.” Any whiff of economic chaos and investors rushed into U.S. Treasuries, since they were viewed as a stable and highly liquid financial instrument that can be easily sold in a crunch. Even during the 2009 Financial Crisis, which originated in the U.S. housing market, investors continued to buy Treasuries.

However, investors are seemingly behaving differently this time. Considerably higher interest rates in the U.S. than the rest of the developed world are not fully enticing them to buy, even during the recent market sell-off. This freak development is worrying. It might indicate that the end of King Dollar is nigh.

Big banks, investment funds, and traders could be dissing American exceptionalism in favor of a more jaded view, since this time the chaos is directly emanating from Washington. Merely escalating uncertainty is raising questions—Trump’s America is seen as less stable and predictable, driving up the risk premium for putting money in the U.S.

The bond market has also seen unusually large price movements. The yield on the 10-year Treasury was just around four percent on April 4, 2025, spiking over the coming week, then settling around 4.5 percent on April 11. Such swings are unusual for the bond market, but analysts differ on what is behind them.

U.S. Treasury Secretary Scott Bessent blamed the spike in rates on deleveraging by hedge fund investors who had borrowed too much employing the “basis trade.” This trade exploits miniscule price differences in the market, but can be upended by large volatility and too much leverage. Yet, there are other, more worrisome explanations.

Since the 1960s American trading partners and investors have fretted about the United States abusing its “exorbitant privilege” and debasing the dollar in a flurry of spending. These worries reached a climax during the 1970s but then gradually subsided, only to reappear during recent crises, such as the Global Financial Crisis and the COVID-19 pandemic. Specifically, the pandemic triggered trillions of dollars in fiscal spending supported by massive monetary injections, breeding fears of a prolonged debasement of the U.S. dollar or even a fiscal crisis in Washington.

During the pandemic the U.S. federal government deficit reached 14.9% of GDP in 2020 and 12.4% of GDP in 2021, astronomical figures only seen during wartime. But as the pandemic subsided the deficit never fully recovered, dropping to 5.5% of GDP in 2022 but then rising again to 6.3% of the country's Gross Domestic Product in 2023 and around 6.4% in 2024. These are figures far beyond the danger line of three percent, indicating too much debt production with debt monetization.

The COVID spending resulted in the biggest bout of high inflation America experienced since the early 1980s. And inflation remains sticky to this day, stubbornly hoovering around three percent. Trump’s volatile trade policies only pour gasoline on this flickering fire of U.S. inflation, justifying a higher risk premium for the dollar as investors look to the future.

Some analysts further speculate that China, a vast holder of U.S. government bonds, could be seeking to dump the dollar as a form of retaliation. But this is unlikely, since it could backfire and wound the Chinese economy. More likely is just less demand for new Treasury issuance, reflecting an aversion in certain quarters to increased U.S. exposure as the country becomes a less reliable global partner. This would include everyone, especially Europe and Japan, not just China.

There are also longer-term policies that are slowly undermining King Dollar. The weaponization of the U.S. dollar via trade, financial, and technology sanctions under both the first Trump and then Biden administrations is chipping away at perceptions of how secure dollar investments are, especially for emerging market economies. Most extreme have been the sanctions levied against Russia by Biden. These froze part of Russia’s reserves and cut the country off from the international payments system based on SWIFT, the Society for Worldwide Interbank Financial Telecommunication. It is therefore little wonder that other large dollar holders, such as China and Saudi Arabia, are reevaluating their exposure and seeking ways to diversify.

Finally, there is the deep irony, in fact paradox contained in Trump’s efforts to turn around the U.S. trade deficit with the world. The U.S. dollar dominates since there is such ample supply of it. America’s exorbitant privilege has a downside: large current-account deficits are needed to meet the global demand for safe assets, such as government bonds. In other words, the U.S. dollar is so dominant because there is so much U.S. debt that the rest of the world can buy. There is simply no alternative to the large, deep, and liquid debt markets of America, virtually creating a monopoly where dollar debt crowds out everything else.

Radically altering this system in one fell swoop with global tariffs and a focus on trade deficits might not totally upend global capital flows, but certainly could be destabilizing and create all sorts of “freak events.” Perhaps this is what investors fear. More of the same, which implies more volatility and policy gyrations. Worst of all would be a so-called “Mar-a-Lago Accord.”

This idea was put forward by Stephen Miran, now the head of the White House Council of Economic Advisers under Trump. Such an accord would aim to dramatically alter global capital flows by permanently devaluing the U.S. dollar via an agreement modelled on the Plaza Accord of 1985. Only this time, U.S. allies, much less China, are unlikely to go along willingly. This raises the specter of a coercive deal forcing other nations to revalue their currencies, putting the United States in a highly adversarial position vis-à-vis the rest of the world.

So far, the Trump administration has dismissed talk of a “Mar-a-Lago Accord.” But any move towards it would amount to a deliberate attempt to erode the dollar’s preeminent position in the global financial system. As a matter of fact, such an accord would likely backfire by raising U.S. borrowing costs, crashing the global economy, and accelerating the search for a replacement to the dollar.

For now, King Dollar still reigns. There is no single viable alternative that could fill its role. But the financial destabilization wrought by Washington is forcing investors to search for diversification. If this trend is sustained, a more fragmented, yet also more multipolar monetary order could emerge with multiple currencies, including crypto currencies, partially supplanting the dollar’s global position. Alas, such a transition would likely be fraught with many more freak events, dislocations, and potential financial crises.