Thanks to President Trump’s new round of international tariffs, the global economy is now at the risk of unraveling. This is not just the result of plunging world trade and investment, but of soaring U.S. military expenditures.

President Trump’s new round of reciprocal and universal tariffs will escalate trade tensions, lower investment, hit market pricing, distort trade flows, disrupt supply chains, and undermine consumer, business and investor confidence. It will certainly penalize global economic prospects.

As fears of a recession mount and mass protests in the U.S. have begun, the loss of over $6 trillion on Wall Street in only two days is just a prelude of what’s to come. Along with China, the large trading economies in Europe, Japan and South Korea, India and Brazil and the rest of the world are positioned to counter the Trump tariffs.

Days before Trump's new tariffs, China declared its trade minister had agreed with Japan and South Korea, Washington’s two treaty allies in Asia, on a common response to Trump’s actions. In Seoul and Tokyo, the statement was seen as overstated. Nonetheless, after the impeachment of former President Yoon Suk Yeol, the divided South Korea must cope with trade war amid a constitutional crisis, whereas Japan’s PM Shigeru Ishiba has declared it a “national crisis.” In South and Southeast Asia, Latin America and sub-Saharan Africa, developing economies coping with natural disasters and external destabilization efforts are targeted by Trump tariffs as well.

As Washington is decoupling the old linkages between trade and defense policies, it has opened the Pandora’s box for multi-dimensional alignments.

US Trade: Allies and Others

Sources US imports: UN; trade deficits, BEA; reciprocal tariff, White House; critical goods, UN

“National security” as pretext for global fragmentation

Taken at face value, the Trump reciprocal tariffs indicate that contemporary America’s greatest threats would be Saint Pierre and Miquelon, Lesotho and Cambodia; that is, a few tiny French islands close to Canada and two poor and small developing countries in Africa and Southeast Asia, respectively.

Ostensibly, the new international tariffs are legitimized by “national security.” In practice, they foster new volatility and uncertainty.

In the past, U.S. military allies were trade partners and vice versa. Now military allies are trade adversaries. In the past, disagreements were resolved while tariffs were reduced; today the reverse applies.

The new protectionism is reminiscent of the Smoot-Hawley and reciprocal tariffs in the 1930s that went hand in hand with assertive nationalism, xenophobia and massive military rearmament paving the way to World War II, the Holocaust, and Hiroshima and Nagasaki. It is thus odd that the military dimension has been largely ignored in recent globalization/deglobalization surveys.

In 1945, the United States accounted for almost half of the global economy. It was the world’s manufacturing giant and greatest debtor. The U.S. dollar monopolized cross-border transactions. Today, the relative share of the U.S. in the world economy has halved. It’s the world’s de-industrial giant and greatest borrower. And the global dominance of the U.S. dollar in world transactions has likely been halved, too.

Military power is an entirely different story, however. It is the muscle that the Biden administration used covertly and the Trump White House likes to tout overtly. It is this brute military primacy that is systematically exploited as the White House seeks to hammer the world into its image.

Military globalization

Global economic integration is often measured by world trade and investment. Thanks to the Trump administration’s mix of reciprocal and universal tariffs, both have been plunging particularly hard since 2017. Ironically, that’s when the world economy was actually positioned for a recovery, but due to the new protectionism, it was missed – and has been missed ever since then.

Though ignored by standard indicators, military expenditures and exports have escalated in two phases since the end of the Cold War which, like World War I initially, was supposed to “bring an end to all wars.” After a brief lull in the 1990s, military expenditures escalated in the 2000s, thanks to the U.S.-led post-9/11 wars, which basically doubled the defense spending while costing the US alone over $8 trillion and almost 1 million deaths in target countries. Following the Obama era, another period of military expansion ensued with the first Trump administration (“Trump 1.0”), escalating dramatically in the Biden years.

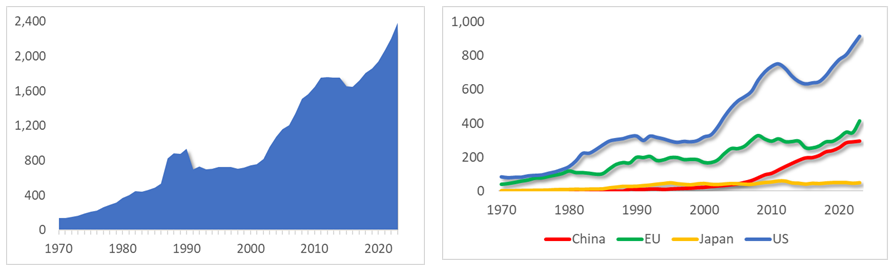

In the process, world military expenditure climbed to a total of $2.4 trillion in 2024. The 6.8% increase in 2023 was the steepest year-on-year rise since 2009. As a result, global spending is now at the highest level ever recorded by SIPRI, the leading research firm in the field. The rise in global military spending can be attributed mainly to the proxy wars in Ukraine and Russia, both armed and financed particularly by the United States, and escalating geopolitical tensions in Asia Pacific, following the U.S. military pivot into the region over a decade ago.

World Military Expenditures (in US$ billions)

Source: SIPRI

U.S. military primacy

As a percentage of world GDP, world trade during “Trump 1.0” fell back to the level where it had been over 15 years before. With reciprocal and universal tariffs, the plunge is likely to prove deeper and more lethal. World investment reflects a similar pattern. As a percentage of GDP, foreign investment inflows, following Trump 1.0, reached a level in 2020 that was first reached 30 years ago.

By contrast, military expenditure does not reflect such trends at all. It has soared. U.S. military spending was $916 billion in 2023. Washington remains by far the largest spender in the world, allocating 3.1 times more to the military than the second largest spender, China. Since the population of China is 4.2 times larger than that of the U.S., the actual difference is far greater. On a per capita basis, Washington spends 12 times more than Beijing in military expenditure.

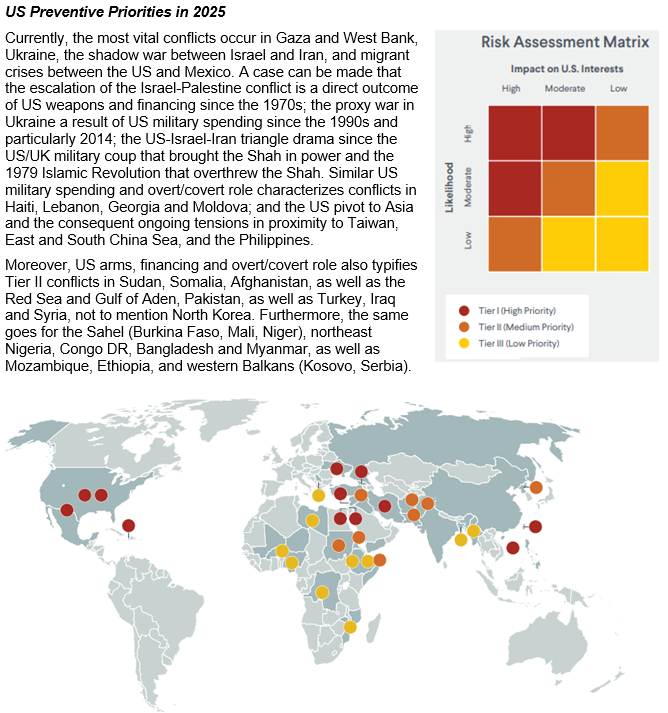

In the Preventive Priorities Survey 2025, U.S. policymaker experts of the Council for Foreign Affairs keep track of priority conflicts, from the perspective of U.S. interests. Yet, most, if not all, of these conflicts originate from and/or have been aggravated by decades of post-Cold War military spending, arms transfers, “advisors” and covert operations by the United States.

Source: CFR, author

Who are the beneficiaries of U.S. military globalization?

Typically, U.S. arms exports grew by 21% between 2015–19 and 2020–24. Meanwhile, its share of global arms exports went from 35% to 43%, which is almost as much as the next eight largest exporters combined. The US supplied major arms to 107 states in 2020–24. US arms exports to European states more than tripled (+233%). States in Asia and Oceania - Japan, Australia, South Korea and Taiwan - received 28% of U.S. arms exports in 2020–24.

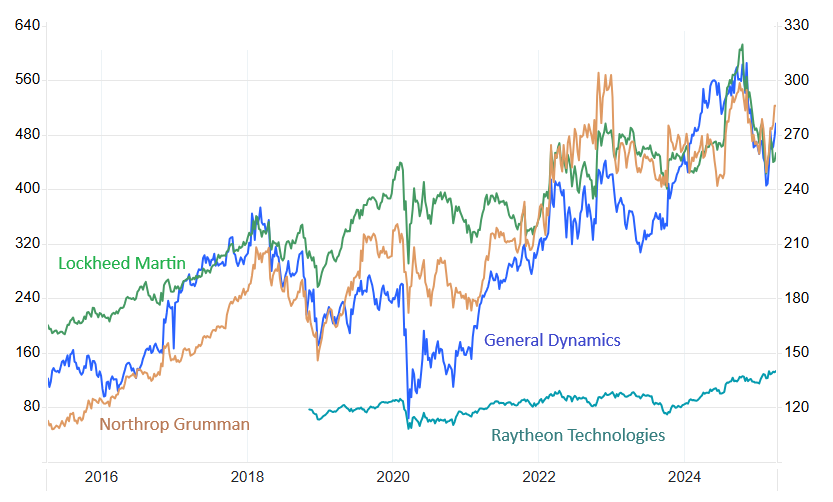

U.S. military primacy has meant windfall profits to a handful gigantic U.S. defense contractors. The Big Defense has been the prime beneficiary, from the proxy war in Ukraine to its counterpart in Gaza and the greater Middle East, and new hot spots emerging from sub-Saharan Africa to Asia. As evidenced by stock prices, the Big Defense has enjoyed colossal profits, particularly in the past half a decade.

US Big Defense: A Decade of Soaring Stock Prices

Source: Tradingeconomics; author, Apr 6, 2025

For all practical purposes, the ongoing rearmament in Asia Pacific is geared to contain China, even at the expense of Asian economic development, which today accounts for more than 60% of global growth prospects.

Combined, U.S. military primacy and the illicit reciprocal and universal tariffs have potential to undermine global economic prospects for years to come. In particular, they could undermine developing economies for decades to come and undermine large emerging economies, which in turn could disrupt global economic growth.

We are amid the most dangerous moment in history since 1933.